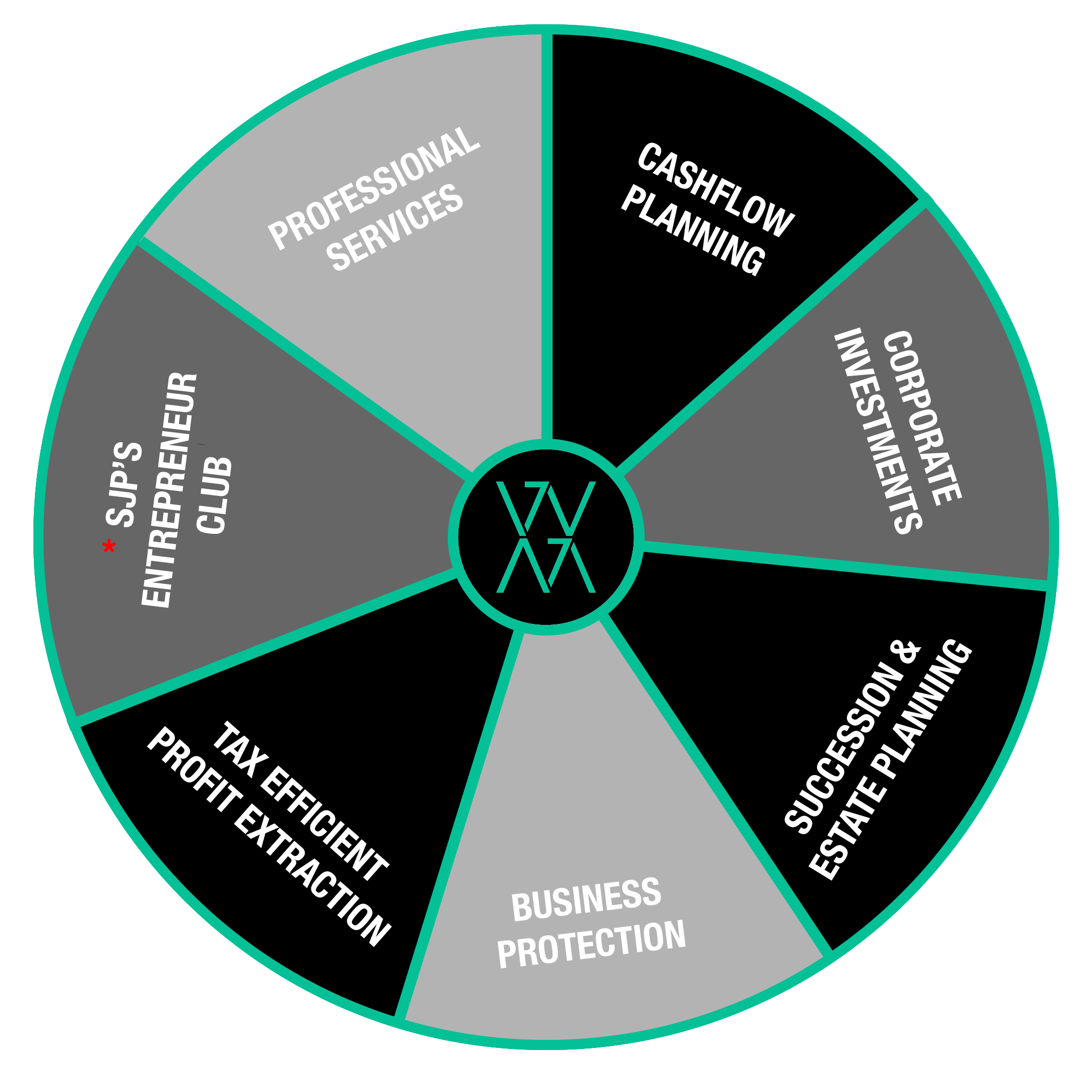

Business Owner Advisory Service

Through our experience, we have built up a comprehensive understanding of the key concerns and challenges that business owners face, and how to successfully address them.

Many business owners invest their time running their business, meaning that their financial affairs can often be neglected.

Here at SeventySeven Wealth Management, we will make it our priority to understand the details of your business, what drives you and your long-term goals, ensuring that whatever decisions you make remain appropriate and continue to meet your objectives.

You may get back less than you invested.

The levels and bases of taxation, and reliefs from taxation, can change at any time. The value of any tax relief depends on individual circumstances.

(*) We work in conjunction with an extensive network of external growth advisers and SME specialists, who have been carefully selected by St. James's Place. The services provided by these specialists are separate and distinct to the services carried out by St. James's Place and include advice on how to grow your business and prepare your business for sale and exit.

Most business owners are familiar with managing their cash flow requirements within their business. A lot of businesses will use cash flow forecasts and projections to make sure that they are constantly on track and will make changes where required. Planning for your financial future on a personal level should be no different.

At SeventySeven Wealth Management, we work with a number of business owners, helping them plan for retirement and beyond. To do this effectively, it is imperative that we take all of your financial affairs into account, to ensure that we can help you to achieve your goals.

As a part of our personalised financial plan, we will use cash flow modelling to help you project forward, building in the various planned events that may happen throughout your life. We are also able to stress test your plan, by inputting unexpected events such as a stock market crash.

Every year, as part of our review, this will be revisited and updated to reflect your current position and give you the opportunity to build in any new goals or aspirations.

We are able to introduce our clients to selected cash management opportunities, where these are appropriate. It should be noted that where a referral is made, the service will be separate and distinct to those offered by St. James's Place.

Keeping your surplus company cash on deposit over the last few years will have meant the capital is unlikely to have grown with inflation. The interest you would have received would also be low. It is easy to forget the damaging effects of inflation. While it does not reduce the monetary value of your capital, it reduces the real value, eroding the spending power of your money in the future. The small amount of interest you receive is also subject to Corporation Tax!

A possible solution for your company is to look to invest surplus capital held on deposit over the medium to long term.

However, following changes to corporate accounting bases, your company may have to value the investment annually and pay Corporation Tax on any increase in value. This will affect your cash flow and increase your accountancy costs.

Therefore, you should take advice when considering making a corporate investment. The investment you choose should then meet two objectives. Firstly, it should have the potential of providing a better return than a deposit account, not only to keep pace with but to beat inflation, and over the medium to long term aim to provide superior investment returns. Secondly, the investment should be structured so that Corporation Tax is only payable on encashment of units and not annually on any increase in value.

The value of an investment with St. James's Place Wealth Management will be directly linked to the performance of the funds selected and may fall as well as rise. You may get back less than you invested.

Entrepreneurial journeys are rarely the same and there are a thousand twists and turns in the road including key concerns and challenges. Guidance may be required at any stage of your business lifecycle, ranging from the start-up of your business all the way through to your exit plan.

There are some tried and tested steps that you should take to keep your business on a firm footing and ensure that you are always ready to take the next step.

At SeventySeven Wealth Management, with the help of The Entrepreneur Club, we are able to help you with the following complimentary support:

- Independent benchmark report, to compare your business both locally and nationally to similar businesses operating in your industry

- Communication programme that is tailored specifically to your needs

- CEO session with a specialist business growth adviser

There are many components involved when running a successful business – marketing, HR, auto enrolment, employment benefits, yet the business itself can be overlooked.

- What would happen if the business owner suddenly died?

- Is the business able to repay any debts if an owner or key employee died?

- What happens if the majority shareholder is diagnosed with a terminal illness?

Most businesses don’t have adequate cover in place for the many business risks that exist. Taking the time to evaluate the impact these risks can have and then protecting against them, can ensure the successful running of your company, without any unnecessary risk to your business or personal wealth.

At SeventySeven Wealth Management we can help you to identify these risks and to put sufficient cover in place, with consideration given to tax-efficiency at every step.

The value of an investment with St. James's Place Wealth Management will be directly linked to the performance of the funds selected and may fall as well as rise. You may get back less than you invested.

When it comes to extracting profits from your Limited company, there are three main routes: salary, dividends and pension contributions. Pension contributions however are often overlooked, even though they can bring significant tax advantages.

Pension contributions can be treated as an allowable business expense and offset against your company's corporation tax bill, so the company could save up to 19%. In addition to this, employers also don’t have to pay National Insurance contributions on these payments. As an individual, there is also potential income tax, dividend tax and National Insurance savings, depending upon how you structure your income.

At SeventySeven Wealth Management, we are able to help you:

- Ascertain how much you can afford to pay into your pension

- Make tax-efficient pension contributions through your company

- Ensure that you are utilising your annual and lifetime allowances

- Give you guidance on how much you will need for retirement

The value of an investment with St. James's Place Wealth Management will be directly linked to the performance of the funds selected and may fall as well as rise. You may get back less than you invested. The levels and bases of taxation, and reliefs from taxation, can change at any time. The value of any tax relief generally depends on individual circumstances.

DismissWhen it comes to operating a business, we understand that there are many requirements to consider, not all of which are financial. We have built up a network of trusted professional advisers so that we can all fully support you with your needs.

Typical services include:

- Legal services

- Accountancy services

- Wills ∓ Powers of Attorney

- Human Resources

We believe in working with these professionals as it allows us to deliver a complete solution, ensuring ease of administration for you, whilst also collaborating to provide the best outcome for your business.

Trusts, Wills and some areas of Inheritance Tax Planning are not regulated by the Financial Conduct Authority. Will writing is a separate and distinct service to those offered by St. James's Place. It should be noted that where a referral is made, the service will be separate and distinct to those offered by St. James's Place.

Whether you are selling your business or handing it over to the next generation, you will need to ensure that your exit is carefully planned, from both a personal and a business perspective.

Many businesses will qualify for Business Relief however what is often overlooked is that if you simply hold these sale proceeds in your bank account, then you will lose this relief. This means that on death, these assets would be included in your estate for Inheritance Tax purposes.

An alternative to this, is to reinvest these funds into a Business Relief qualifying asset, using the replacement property provision rules. This would allow you to benefit from an immediate Inheritance Tax exemption, meaning that your family would inherit 100% of these funds.

There are many other considerations such as this example which is why we urge you to take expert advice in this area.

Don’t invest unless you’re prepared to lose all the money you invest, This is a high risk investment and you are unlikely to be protected if something goes wrong.